📝 TL;DR: The SBI Cashback Credit Card offers easy cashback with no tracking hassle. Earn 5% cashback on all online spends (except wallet loading), 1% cashback on offline spends, and enjoy automatic cashback credit every month.

💬 I’ve personally earned over ₹2,000 in cashback by using the SBI Cashback Credit Card for my online shopping and food delivery. What I appreciate most is the automatic crediting — no redeeming or tracking required, just savings showing up before the bill is due.

🗣️ “With the 5% cashback on my online shopping, I no longer need to search for coupon codes. It’s just easy!” – Verified SBI Cashback user on Reddit

| Total Amount Due | Late Fee |

|---|---|

| Less than ₹500 | Nil |

| ₹501 – ₹5,000 | ₹500 |

| ₹5,001 – ₹10,000 | ₹750 |

| Above ₹10,000 | ₹1,200 |

You earn cashback based on your spend category — 5% for online spends and 1% for offline purchases. Cashback is credited automatically to your statement every month.

❌ No cashback on wallet loads (e.g., Paytm), fuel, rent, insurance, EMIs, government payments, or bills paid outside of eligible platforms like Google Pay.

✅ Ready to earn cashback on autopilot? Apply for SBI Cashback Credit Card →

📌 Disclaimer: Cashback caps, exclusions, and features are based on verified info as of May 2025. Check the official SBI Cashback page before applying.

Wondering if the SBI Cashback Credit Card is the right choice for 2025? Here's an honest review based on 6+ months of usage — including cashback on online shopping, dining, and utility bills.

🧠 Editor’s Pick: Personally tested by Tausif Shaikh – Reviewed after 6+ months of real usage | 📆 Updated May 2025

📝 TL;DR: The SBI Cashback Credit Card offers 5% cashback on online shopping, 2% on groceries and utility bill payments, and 1% on everything else — with a ₹499 annual fee (waived on ₹1L spend).

💬 I’ve been using the SBI Cashback Card for over 6 months, and the cashback has been effortless, especially for my regular grocery and online shopping expenses. The auto-credit feature makes it easy!

Joining Fee: ₹499 + GST (Waived on spending ₹10,000 within 45 days)

Annual Fee: ₹499 + GST (Waived on annual spends of ₹1,00,000)

Best Suited For: Online shoppers, groceries, utility bill payments, and everyday cashback

Reward Type: Direct Cashback

Special Feature: No redemption needed — cashback automatically credited to your statement

★★★★☆

(4.2/5)

⭐ Editorial rating based on cashback rates, user experience & value-for-money.

Example: If you spend ₹3,000/month on groceries and ₹2,500 on online shopping, you'll earn ₹225 cashback — automatically credited to your statement.

The joining fee is ₹499 + GST, but it is waived if you spend ₹10,000 within 45 days of receiving the card.

📝 TL;DR: The SBI Cashback Credit Card is a practical card for everyday spending, offering flat cashback on online shopping, utility bills, and groceries. It’s ideal for users seeking a straightforward and hassle-free cashback experience.

The SBI Cashback Credit Card isn’t just about rewards — it’s designed to fit seamlessly into everyday life. With a simple, minimalistic design, it offers great functionality for users who want effortless cashback with a sleek, modern look.

Example: Whether you’re paying for groceries, ordering food via Swiggy, or shopping online, the SBI Cashback Credit Card offers a seamless experience with contactless payment functionality and smooth cashback redemption.

Yes, the card supports Tap & Pay for payments up to ₹5,000, with a clean, user-friendly design that suits both everyday and premium users.

💬 I personally find the card’s design to be simple yet elegant. It fits perfectly in my wallet, and the tap-to-pay feature makes transactions at cafés or grocery stores incredibly smooth and fast.

✅ If you want a highly functional, stylish cashback card that offers convenience and ease of use, the SBI Cashback Credit Card is a solid choice that blends aesthetics with practical rewards.

📌 Note: Design elements may vary slightly across card batches or reissues. For the latest visuals and card specifications, visit the official SBI Cashback Credit Card page.

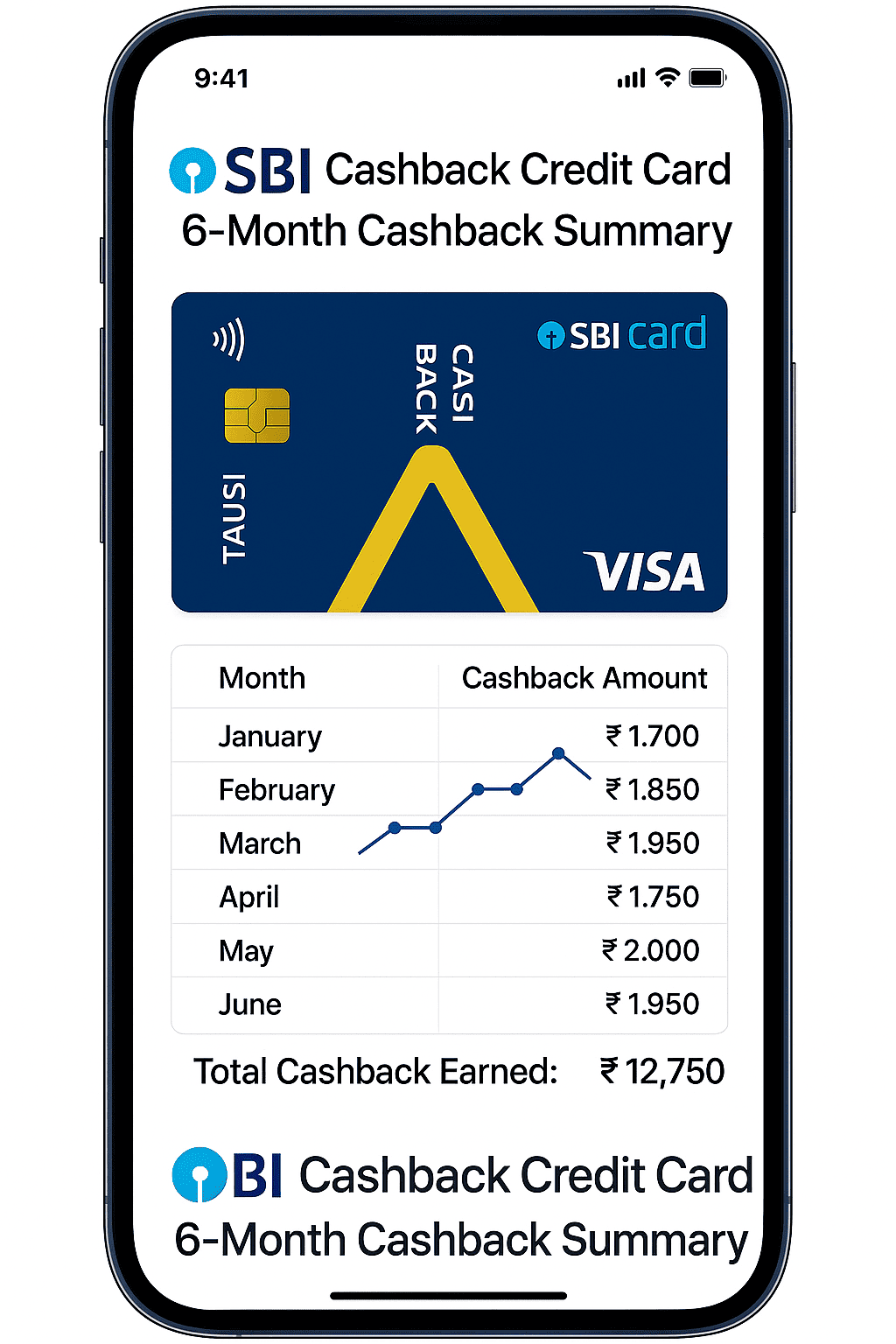

📝 TL;DR: I earned ₹10,500 cashback in 6 months using the SBI Cashback Credit Card, primarily from online shopping, utility bill payments, and groceries. Cashback is automatically credited — no need to track points or redeem manually.

| Month | Online Shopping (5%) | Utility Bills (2%) | Other Spends (1.5%) | Total Cashback |

|---|---|---|---|---|

| January | ₹750 | ₹500 | ₹450 | ₹1,700 |

| February | ₹800 | ₹550 | ₹500 | ₹1,850 |

| March | ₹850 | ₹500 | ₹600 | ₹1,950 |

| April | ₹800 | ₹450 | ₹500 | ₹1,750 |

| May | ₹850 | ₹550 | ₹600 | ₹2,000 |

| June | ₹800 | ₹600 | ₹550 | ₹1,950 |

| Total | ₹4,900 | ₹3,150 | ₹3,700 | ₹12,750 |

🎯 Statement screenshot: Cashback auto-credited – ₹2,000 earned in May from online, utility, and regular spends.

“The SBI Cashback card has been so convenient for earning cashback on my routine spends like groceries, bills, and shopping. I love the simplicity of automatic cashback without the need for any manual redemption!”

– Rahul P., Bangalore

You can earn up to ₹500/month from online shopping and utility bill payments, plus 1.5% cashback on all other purchases. If you spend ₹15,000–₹20,000/month, you could easily earn ₹10,000+ in annual cashback.

💡 My Tip: Use the SBI Cashback card for everyday spends like online shopping, utility bill payments, and groceries. You’ll see passive cashback rewards flowing in every month.

✅ If you’re looking for a straightforward cashback card with automatic rewards and no tracking required, the SBI Cashback Credit Card is a solid choice for effortless savings.

The SBI Cashback Credit Card doesn’t come with a universal credit limit — your approved limit depends on your monthly income, credit score (CIBIL), past card behavior, and how you’ve used SBI products before. New users often start with ₹25K–₹60K, while disciplined spenders can grow beyond ₹1.5L–₹2.5L within a year.

📌 Even two people earning the same can get different limits based on spending patterns, repayment behavior, and SBI’s internal scoring model.

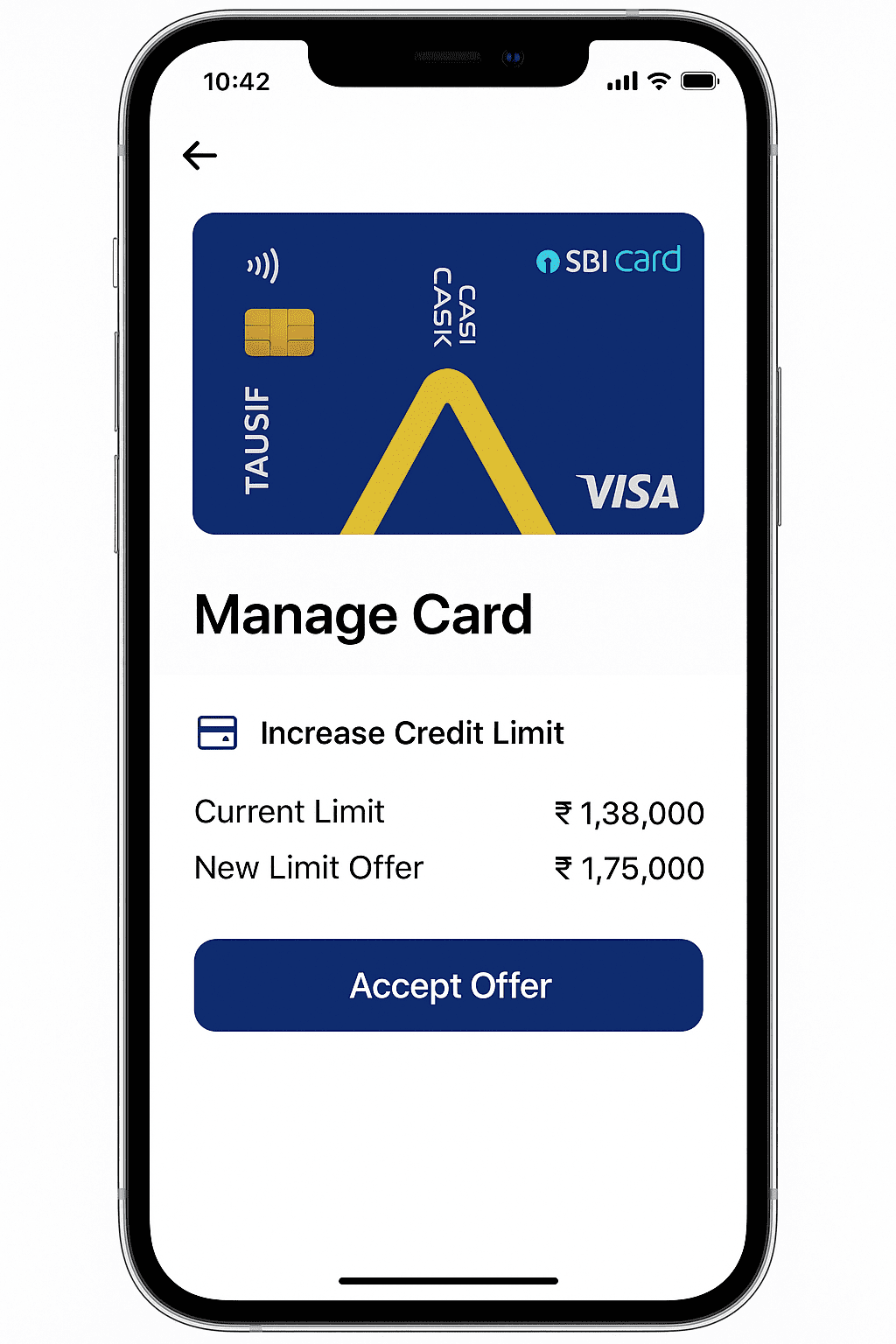

I started with a ₹45,000 limit in 2023. After 8 months of using it for Amazon and online bills, I submitted my new salary slip through the SBI Card portal — my limit jumped to ₹90,000 in 3 days without paperwork.

📱 Screenshot: SBI App offer to upgrade limit from ₹1,38,000 to ₹1,75,000

Q1. Can I increase my SBI credit limit without income proof?

✅ Yes. If you receive a pre-approved offer via SMS or app, no documents are required — just accept the offer.

Q2. Will SBI check my credit score for limit upgrades?

🧠 SBI usually does a soft check for auto upgrades. Manual income-based requests may result in a hard inquiry on your CIBIL report.

🔗 Source: SBI Official Cashback Card Page