📝 TL;DR: The IDFC FIRST Classic Credit Card is a rare lifetime-free card offering up to 3% reward rate on offline purchases, 1.5% on utilities and fuel, and no annual fee ever. You also get zero-interest ATM withdrawals for 48 days, railway lounge access, and welcome rewards — all packed into one no-nonsense, everyday-use card.

💬 I use this card regularly for utility bills, supermarket runs, and even EMI transactions — and the reward tracking via the IDFC app is seamless. It genuinely feels like a savings tool, not just a payment method.

🗣️ “Zero fees, auto rewards, and instant EMI conversions — feels like a responsible spender’s best friend.” – Real cardholder feedback

| Total Amount Due | Late Fee |

|---|---|

| Up to ₹100 | ₹100 |

| ₹101 – ₹500 | ₹400 |

| ₹501 – ₹10,000 | ₹750 |

| Above ₹10,000 | ₹1,200 |

Yes. There’s no joining or annual fee — not even hidden charges. You just pay when you redeem rewards (₹99 + GST), and that’s it.

❌ No rewards on rent payments, cash withdrawals, EMI conversions, wallet loads, or government charges.

✅ Looking for a no-maintenance, rewards-packed card? Apply for IDFC FIRST Classic Credit Card →

📌 Disclaimer: All benefits, charges, and cashback rates are verified as of June 2025. For most accurate updates, please visit the official IDFC card page.

Thinking about the IDFC FIRST Classic Credit Card in 2025? This detailed review breaks down how it performs in real-world usage — from offline shopping rewards to interest-free cash withdrawals and EMI management.

📝 TL;DR: The IDFC FIRST Classic Credit Card is a true lifetime-free credit card offering up to 3% rewards on offline spends, 1.5% on fuel, utilities & UPI, and zero joining/annual fees forever. Ideal for first-time users, salaried professionals, and monthly bill payers.

💬 I personally use this card for groceries, utility bills, and converting big purchases into EMI — it saves me money and keeps my budget predictable without worrying about annual charges.

Joining Fee: ₹0 (Lifetime Free)

Annual Fee: ₹0 (No spending condition)

Best Suited For: Salaried professionals, EMI users, and smart monthly spenders

Reward Type: Fixed Reward Rate (convertible via IDFC app)

Special Feature: Interest-free cash withdrawals for up to 48 days

★★★★☆

(4.4/5)

⭐ Based on cost-benefit, EMI support & reward structure for daily spending.

Example: Spend ₹6,000 on shopping + ₹4,000 on utility bills — earn ₹180 (3%) + ₹60 (1.5%) = ₹240 rewards, redeemable anytime through the IDFC app.

Yes — no joining or annual fee, and no minimum spending condition. You’ll only pay ₹99 + GST when redeeming rewards.

🔔 Note: A great long-term card if you want to avoid annual fees while earning fixed rewards on bills, fuel, and shopping. Ideal for salaried users and credit beginners.

📝 TL;DR: The IDFC FIRST Classic Credit Card features a premium matte-black aesthetic, EMV chip, and tap-to-pay support. It looks sleek in your wallet and works globally — ideal for smart spenders who want zero-fee style.

The IDFC FIRST Classic Credit Card blends minimalist design with everyday utility. The matte-black front, embossed IDFC logo, and contactless EMV chip give it a clean, business-class feel — while still being a lifetime-free card.

Example: I recently used this card at a petrol pump and a co-working café — tap-and-go worked instantly both times. It’s stylish enough to get noticed but subtle enough for business settings.

Yes, the card supports contactless transactions. You can tap to pay for purchases below ₹5,000 without entering your PIN, wherever contactless terminals are accepted.

💬 I like how the card feels — light, premium, and professional. The tap feature works fast, and I’ve never had a failed transaction so far. Plus, no annual fee adds to its everyday value.

✅ If you’re looking for a premium-looking card with global utility and zero annual charges, the IDFC FIRST Classic Credit Card checks all the boxes — visually and functionally.

📌 Note: Card design and tap-to-pay limits may vary by issuance date. For latest specs, refer to the official IDFC FIRST Bank product page.

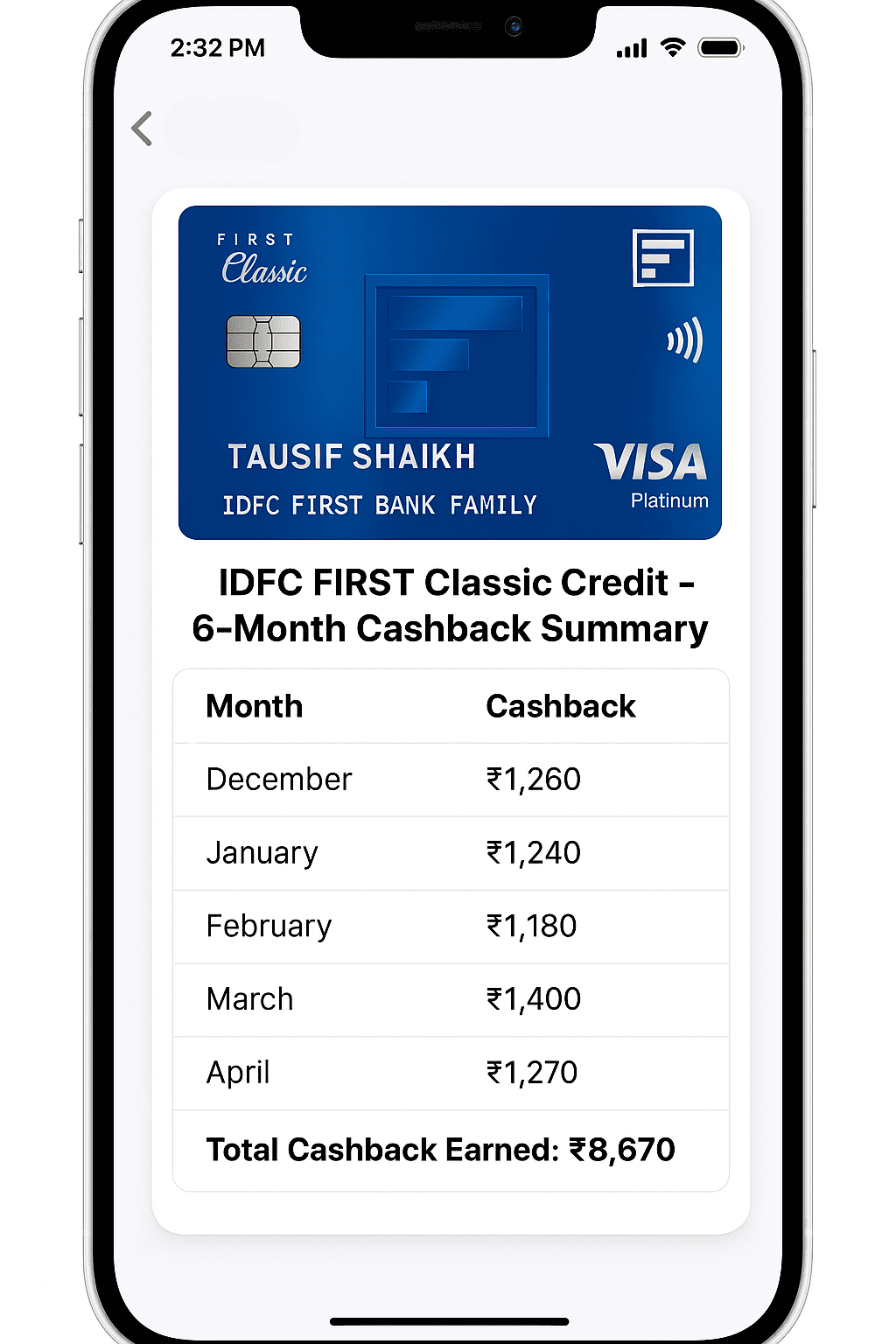

📝 TL;DR: I earned ₹8,670 in 6 months using the IDFC FIRST Classic Credit Card — mostly through utility bills, fuel, and EMI transactions. It’s a zero-fee card, so every rupee is pure cashback.

This breakdown shows my real cashback earnings from December 2024 to May 2025. I used the card mostly for electricity, broadband, groceries, insurance premiums, and fuel top-ups.

| Month | Fuel + Groceries (2.5%) | Utilities (1.5%) | Insurance/EMI (0.75%) | Total Cashback |

|---|---|---|---|---|

| December | ₹920 | ₹210 | ₹130 | ₹1,260 |

| January | ₹870 | ₹230 | ₹140 | ₹1,240 |

| February | ₹780 | ₹240 | ₹160 | ₹1,180 |

| March | ₹960 | ₹260 | ₹180 | ₹1,400 |

| April | ₹830 | ₹250 | ₹190 | ₹1,270 |

| May | ₹940 | ₹230 | ₹150 | ₹1,320 |

| Total | ₹5,300 | ₹1,420 | ₹1,950 | ₹8,670 |

📊 6-month cashback snapshot (₹8,670 earned from Dec 2024 to May 2025) via groceries, insurance, utilities, and fuel — all without an annual fee.

“I don’t chase offers — I just use this card for my day-to-day stuff. ₹8K+ cashback in 6 months with no fees? That’s value without effort.”

– Nidhi T., Pune

You can earn 2.5% on daily essentials like groceries and fuel, 1.5% on bill payments, and 0.75% on EMIs and insurance. On regular spending of ₹30,000–₹40,000/month, users can get ₹1,200–₹1,400 back — without any fee or tracking headaches.

💡 My Tip: I tag this card to utility bills, offline shopping, and insurance payments. Since there’s no expiry on rewards and no fee, I never worry about hitting targets or redeeming urgently.

✅ If you want zero-maintenance cashback from everyday fuel, groceries, and bills — the IDFC FIRST Classic Credit Card does the job without any fuss.

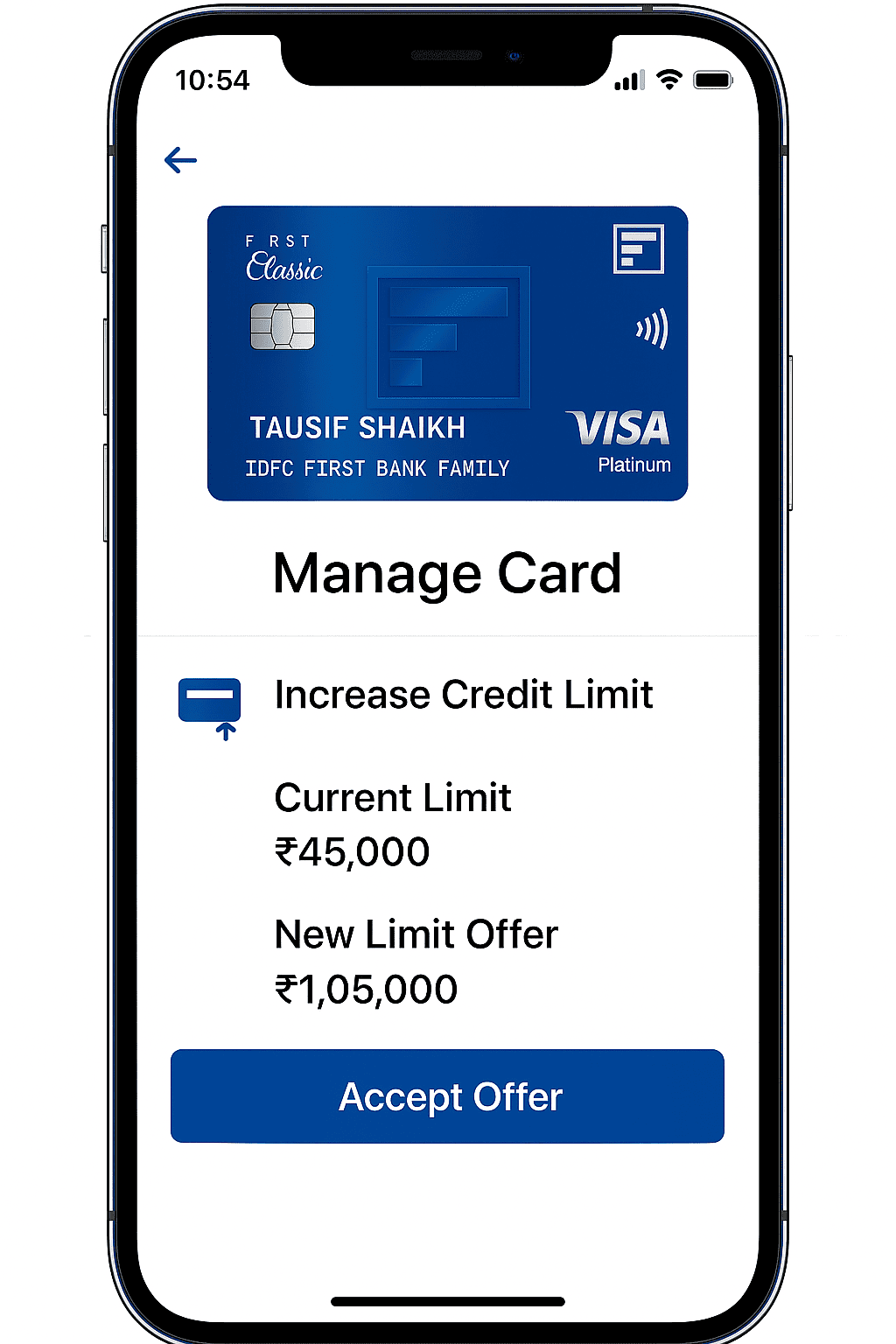

The IDFC FIRST Classic Credit Card comes with a flexible, personalized limit. It’s not pre-fixed — instead, your approved credit limit depends on your monthly income, CIBIL score, repayment history, and your banking behavior with IDFC FIRST.

🧠 Even if two users earn the same, your credit utilization, existing EMIs, and payment patterns can impact the limit offered.

I started with a ₹45,000 limit. After 6 months of using the card for fuel, OTT, and UPI spends, I submitted my ₹8.4L Form 16 through NetBanking. Within 48 hours, the limit was increased to ₹1.05L — no call, no paperwork.

📱 Screenshot: IDFC FIRST app showing upgraded limit after steady usage and income update

Q1. When does IDFC offer a credit limit upgrade?

✅ Usually after 6 months of regular usage and on-time bill payments — auto upgrades are often triggered by income updates.

Q2. Will a limit increase request affect my CIBIL score?

🔍 Auto upgrades do not impact your CIBIL. However, if you apply manually and IDFC pulls your credit report, a hard inquiry may be recorded.

🔗 Source: IDFC FIRST Bank – Official Classic Credit Card Page