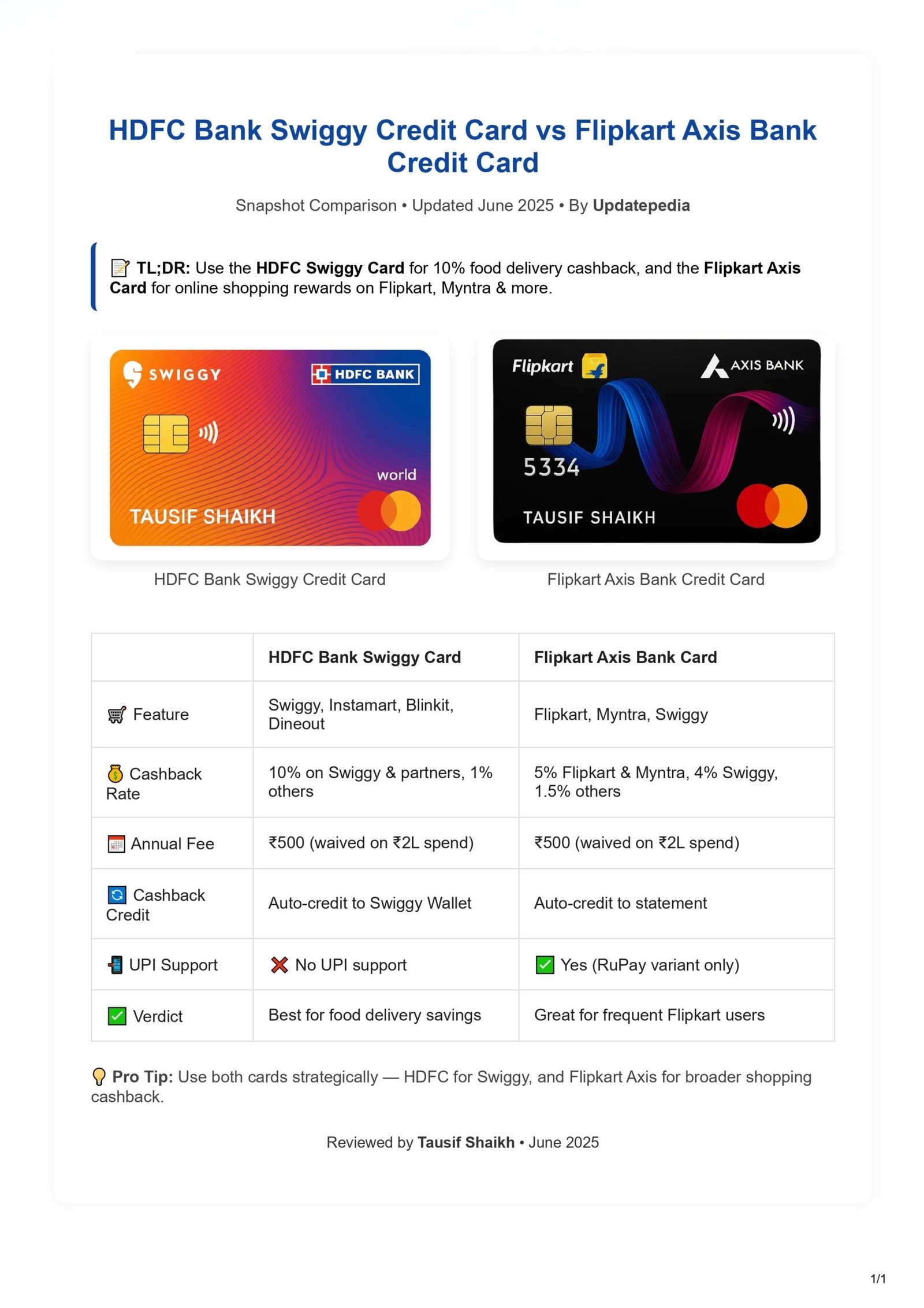

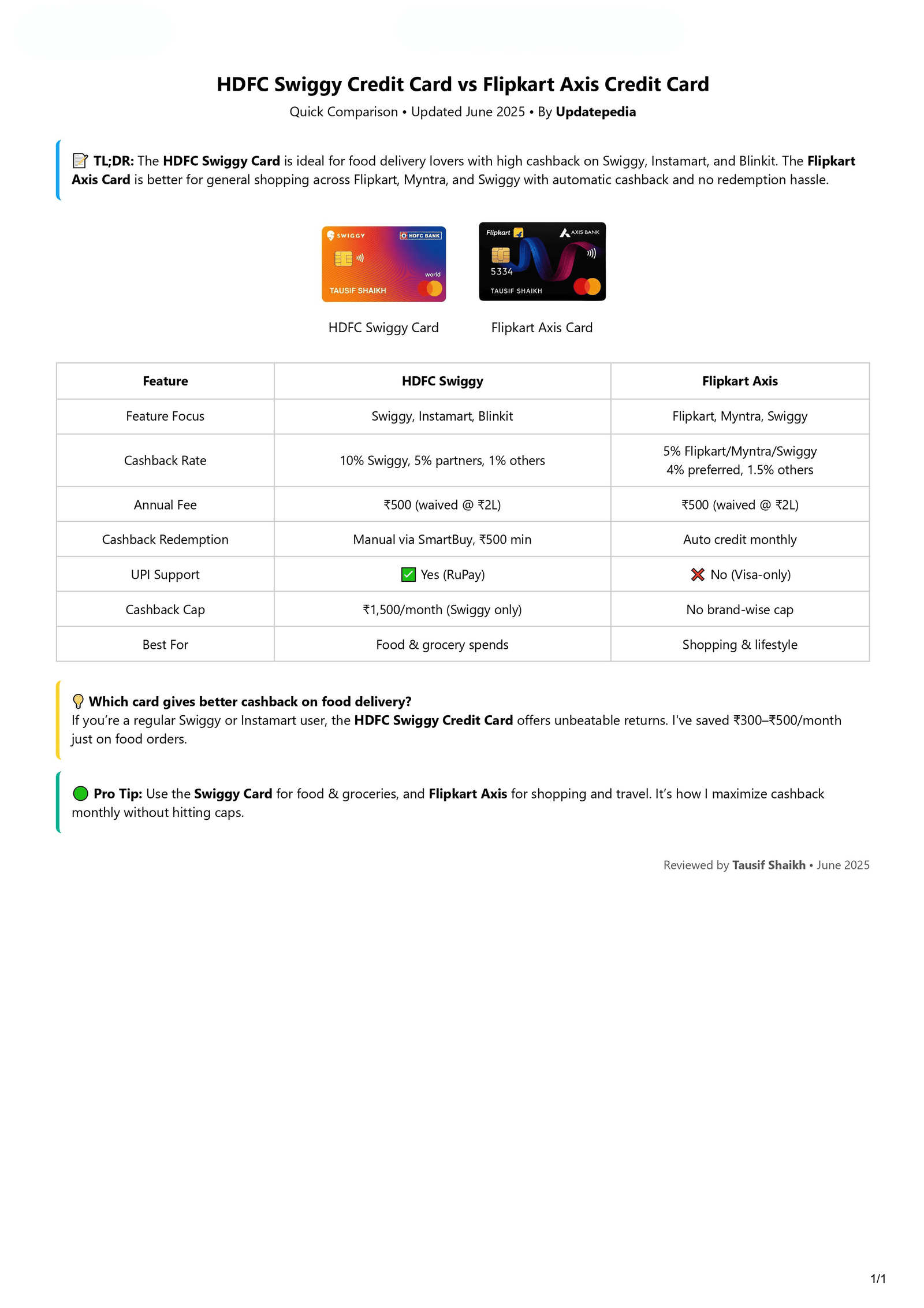

Here’s a quick visual comparison of the key features of the HDFC Bank Swiggy Credit Card and Flipkart Axis Bank Credit Card — from cashback rates to UPI support — all in one glance. Ideal for quick decision-making or sharing with friends. For more details, you can visit the official HDFC Bank Swiggy Credit Card page or the official Flipkart Axis Bank Credit Card page.

📝 TL;DR: The HDFC Bank Swiggy Credit Card is perfect for foodies and Swiggy users with a 10% cashback on Swiggy orders and partner brands. The Flipkart Axis card, on the other hand, offers 5% cashback on Flipkart, Myntra, and Swiggy. If you’re a frequent food delivery user, the HDFC Swiggy card gives you more value, but if you shop often across multiple platforms, the Flipkart Axis card is more versatile.

🖼️ Share this chart or download the 1-page PDF summary.

Reviewed by Tausif Shaikh | Credit Card Expert & Blogger | Verified June 2025

As a credit card expert with years of experience reviewing financial products, I’ve noticed that both cards cater to distinct user needs. The HDFC Swiggy Credit Card is great for those who prioritize food delivery, offering excellent cashback on Swiggy and partner brands. On the other hand, the Flipkart Axis Bank Credit Card is better for users who frequently shop online across various e-commerce platforms, offering cashback on Flipkart, Myntra, and Swiggy purchases.

For example, if you spend ₹10,000 on Swiggy using the HDFC Swiggy Credit Card, you would get ₹1,000 cashback (10%). On the other hand, if you make the same purchase using the Flipkart Axis Bank Credit Card, you’d receive ₹500 cashback (5%) on Swiggy orders. However, for general online shopping, the Flipkart Axis card offers cashback on a variety of platforms, whereas the HDFC Swiggy card is focused on food-related purchases.

HDFC Swiggy Credit Card offers 10% cashback on Swiggy and 5% on Zomato, Instamart & Blinkit — credited as a bill adjustment in the next cycle. Flipkart Axis Credit Card gives 5% cashback on Flipkart and Myntra, 4% on Swiggy, Cleartrip, PVR, and 1.5% elsewhere — cashback reflects in the monthly statement.

Personally, I find Flipkart Axis’s 1.5% flat cashback handy for regular spends, while HDFC Swiggy’s food-specific perks are unbeatable if you’re a frequent foodie.

| Feature | HDFC Swiggy Credit Card | Flipkart Axis Credit Card |

|---|---|---|

| Redemption Type | Auto-adjusted in statement | Direct cashback credit |

| Timeline | Next billing cycle | Same cycle (within statement) |

| Manual Action Needed | ❌ None | ❌ None |

👉 Snapshot Verdict: Love ordering food? HDFC Swiggy is your go-to. Want an all-rounder card with Flipkart & travel rewards? Go with Flipkart Axis.

💡 Tip #1: Use the Flipkart Axis Card for online shopping and travel bookings. For food delivery, I recommend using the HDFC Swiggy Card to maximize the 10% benefit.

💡 Tip #2: Regularly check your card provider’s mobile app for real-time cashback tracking and avoid surprises at billing time.

💼 Pro Tip: Want to maximize savings? Use Flipkart Axis Card for all online shopping and travel bookings. Then switch to HDFC Swiggy Card for all food orders and Instamart runs. That way, you unlock both categories efficiently without needing to redeem anything manually.

✅ Fact Check: Redemption process verified from HDFC Bank Swiggy Card T&Cs and Axis Bank Flipkart Credit Card details as of June 2025.

🧑⚖️ Reviewed By: Tausif Shaikh, Finance Blogger • Updated on: June 10, 2025

Flipkart Axis charges ₹500/year; Swiggy HDFC charges ₹500 too. This calculator shows how long it’ll take to recover the fee with your monthly food and shopping spends. If you’re a regular Swiggy user like me, HDFC’s 10% cashback stacks up quickly!

Curious how much you need to spend monthly to break even? Enter your average food and shopping expenses below. We’ll instantly show breakeven timelines based on real cashback rates.

Want more details? Visit

HDFC Swiggy Card page or

Flipkart Axis Card info.

![]() Flipkart Axis: --

Flipkart Axis: --

![]() HDFC Swiggy: --

HDFC Swiggy: --

🔍 Note: Enter monthly food and brand spending separately. The calculator assumes cashback is auto-credited without exclusions.

✅ Fact Check: Cashback logic and brand partners are verified from Axis and HDFC Bank card pages, accurate as of June 2025.

🧑⚖️ Reviewed By: Tausif Shaikh, Finance Blogger • Updated on: June 9, 2025

| Card | Why It’s a Great Alternative |

|---|---|

SBI Cashback Credit Card

SBI Cashback Credit Card |

✅ Flat 5% cashback on most online merchants ✅ Ideal for Amazon, Nykaa, AJIO, BigBasket ❌ Excludes rent, wallets, fuel, and insurance |

Axis Bank ACE Credit Card

Axis Bank ACE Credit Card |

✅ 5% cashback on utility bill payments via Google Pay ✅ 4% on Swiggy, Zomato, Ola + 2% elsewhere 💰 ₹499 annual fee (waived on ₹2L/year spend) |

Amazon Pay ICICI Credit Card

Amazon Pay ICICI Credit Card |

✅ Lifetime free with 5% cashback for Prime members ✅ Cashback auto-credit as Amazon Pay balance ✅ Good for daily Amazon + utility + wallet payments |

💡 Tip: These cards cover more generic spending needs. If your monthly spend isn’t limited to Flipkart or Swiggy, pairing one of these with a category card makes your cashback strategy more balanced.

👎 Who should avoid these? If you mostly shop on Flipkart or order from Swiggy multiple times a week, stick to HDFC Swiggy or Flipkart Axis — those cards offer much higher targeted rewards.

✅ Fact Check: Card benefits and terms verified from official SBI, ICICI, and Axis Bank sites as of June 2025.

🧠 Reviewed by Tausif Shaikh, Credit Card Blogger | Updated: June 2025